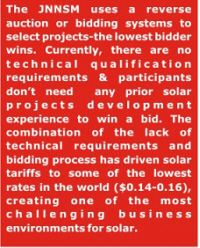

|

The solar industry has immense potential for a tropical

country like India where around 45% of households, mainly rural ones, do not

have access to electricity, says our new research. The industry has witnessed

rapid growth over the past few years and is projected to grow further in future.

India is blessed with ample solar radiation and most part of

the country receives 300 to 330 sunny days in a year. India receives solar

energy equivalent to more than 5,000 Trillion kWh per year, which is far more

than its total annual energy consumption. The countrys geographical location,

large population and government support are assisting it to become one of the

most rapidly emerging solar energy markets in the world.

However with all this positives, the industry didnt grow

as expected last year.

Due the election year there was a complete policy paralysis

in the Government & the priorities were changed.

The report provides an insight on various small & Mid

level companies forming the major chunk of solar industry in India. It

thoroughly examines current industry trends, with focus on recent changes in the

state and country level regulatory environment. The report will assist investors

to understand the market dynamics and get an insight into the future outlook of

solar power market in India.

Many states have started promoting solar based applications

by giving incentives and tax savings. States like Gujarat and Rajasthan have

formulated transparent and progressive regulatory framework in order to boost

the solar industry. Besides, states like Uttar Pradesh, West Bengal, Maharashtra

and Chandigarh are promoting solar energy in rural, urban and semi urban areas.

More recently Madhya Pradesh has joined the Solar Promotion bandwagon.

The forecast given in this report is not based on a complex

economic model, but is intended as a rough guide to the direction in which the

market is likely to move. This forecast is based on correlations between past

market growth, growth of base drivers and possible impact of recession in the

economy and support provided by various State Governments.

While most Indian state have followed the lead of JNNSM in

terms of policy and guidelines, the state of Gujarat decided to go the

feed-in-tarriff route. A total of 930mw have been installed year-to-date(2012)

of which 635mw were installed in Gujarat.

Here is a brief of what various states have achieved :

GUJARAT

: 824mw of solar projects have been installed under the Gujarat state solar

Policy, with 379mw delayed. These 379mw projects will receive newly announced

Oct 2012 tariffs(levelised tariff for 25 years is Rs 10.37 (~$0.19)/kWh for PV

Projects) which are about 20 per cent lower compared to 2011 tariff levels.

Though Gujarat announced tariffs for 2012-15, it does not have any plans to

announce any targets or installation goals. GUJARAT

: 824mw of solar projects have been installed under the Gujarat state solar

Policy, with 379mw delayed. These 379mw projects will receive newly announced

Oct 2012 tariffs(levelised tariff for 25 years is Rs 10.37 (~$0.19)/kWh for PV

Projects) which are about 20 per cent lower compared to 2011 tariff levels.

Though Gujarat announced tariffs for 2012-15, it does not have any plans to

announce any targets or installation goals.

KARNATAKA : To achieve commercial viability and

expeditiously operationalize the Renewable Energy Projects. to enhance the

contribution of Renewable Energy in the total installed capacity of the state

from 2400 MW to about 6600 MW by 2014. To conserve 7901 MU (900 MW) by 2014

through the Energy Efficiency & Energy Conservation measures in all sectors.

The KREDL MD Mr. Balram (IAS) seems to be in no hurry to

commence the projects It seems all the money which KREDL collected thru earnest

money is being used to fund KREDL. (Just a doubt), There are no updates as to

whether PPAs were signed or if financial closure was reached. The Karnataka

Renewable Energy Development Agency has also submitted recommendations to the

state to develop 1.000GW of Solar Energy in five years or 200MW per year. KREDL

willing.

RAJASTHAN : The state of Rajasthan has sanctioned and

installations is either completed or underway for 730 MW of solar projects

currently.

ORISSA : The Orissa Renewable Energy Agency (OREDA)

called for tenders auctioned off a 54MWp. The project includes Installation of

Grid Connected Rooftop Solar Photovoltaic Power Plants with aggregate 54 MWp

capacity in various States across the Country on Pilot Basis. The project aims

to reduce the fossil fuel based electricity load on main grid and make the

buildings self-sustainable to the extent possible.

Projects can be set up on the concept of Net Metering/

Feed-in-Tariff on Pilot Basis. The individual project will normally range from

10 kW to 500 kW size. The projects below 10 kW may also be considered for

residential sector. the lowest recorded bid in India. OREDA plans to call a

tender to develop another 45mw in the next few weeks.

MADHYA PRADESH : Madhya Pradesh Power Management Company

Limited has recently signed PPAs for 225mw of PV projects with five project

developers under a reverse auction mechanism. Those going in for MNRE subsidy

ware in for a rude shock as subsidy schemes were discontinued and crore&

cores of money of various company stuck. There is an utter confusion as

customerstillsites MNRE guidlelines where vendor wondor how to convince. Madhya

Pradesh also recently announced a solar policy to fulfill its RPO obligations

with 150 Mwcommisioned thru Welspun.

MAHARASHTRA : Maharashtra State Power Generation Company

Limited(MahaGenco) has 150MW of solar power projects under development by three

companies. State plans to develop a 100MW project in Usmanabad district, 25mw in

Parbhani district and 125MW in Yavatmal district are in very early stages of

planning.

JHARKHAND : Based on RPO Policy, the state is targeting

300 MW of solar power projects to be developed in the next future. Off this 200

MW has already been auctioned.

UTTAR PRADESH : The Uttar Pradesh New and Renewable

Energy Development Agency recently released its drafts solar policy. The state

has set a goal to achieve 1,000 MW of solar installations by march 2017. The

draft was to be submitted for cabinet approval on September 13, 2014 and may

take another month or more for the policy to come into effect.

Solar market too has become highly fragmented both

product-wise as well as number of companies jumping into the Solar bandwagon.

Vikram Solar completed 5MW in Tamilnadu in a record time. Waaree Energies Ltd.,

a Mumbai based PV Manufacturer has taken huge projects in Gujarat and even plans

to invest 800 crores in MP.

Vikram Solar has just completed 5MW in Tamilnadu in a record

time. Waaree Energies Ltd., a Mumbai based PV Manufacturer has taken huge

projects in Gujarat and have started acquiring smaller solar companies having

strong Solar experience. Swelect Energy Systems Ltd, formerly Numeric Power

Systems Ltd, a BSE listed company sold of its UPS Business Unit for over 850

crores to concentrate on Renewable Energy, space.

In just a few months the company has set up and commissioned

two solar Power Plants and a Wind Power Plant and has over 1645 rooftop

installations to its credit. Consul is in the process of acquiring Megatech

& now Neowatt which Integrates as well as manufactures SPCU which has IEC

certifications

A 12.8 GW opportunity till 2016 - the Indian solar market is

a key future growth market for PV :

Indias installed capacity as of quarter ending 31 March

2014 was 2.63 GW, which is still negligible as compared to more mature markets

such as Germany. However, the first two quarters of 2014 alone have seen

additions of 657.22 MW to Indian PV installed capacity, showing the

lacklustreness of the market. The market is currently mostly driven by FiTs. By

introducing the solar Renewable Purchase Obligations (RPOs) and the solar

Renewable Energy Certificate (REC) mechanism, the government has created a

further market instrument to advance solar power in India.

Further, the falling cost of solar will lead to new projects

in the captive commercial space as solar tariffs become competitive with

commercial and industrial grid prices in various parts of the country.

There are also external factors in India challenging its

solar industry, namely high inflation and consequently high interest rates,

slowdown in GDP growth, a several depreciated rupee and relentless corruption

scandals of the previous Govt. Low bids with high interest rates in the range of

13 to 15 per cent make it challenging to borrow in India (most Indian Banks look

at these projects as risky.) and successfully execute a quality project that can

last 25 years. The rating does not include major players such as BHEL, BEL, CEL,

TATA BP Solar India Limited, Solar Semi-conductor & Moser Baer India

Limited, LANCO, L&T, INDO SOLAR, Reliance Power, Mahindra Power, Wipro-ECO

etc. Limited has recently signed Piven by FiTs. By introducing the solar

Renewable Purchase Obligations (RPOs) and the solar Renewable Energy Certificate

(REC) mechanism, the government has created a further market instrument to

advance solar power in India. There are also external factors in India challenging its

solar industry, namely high inflation and consequently high interest rates,

slowdown in GDP growth, a several depreciated rupee and relentless corruption

scandals of the previous Govt. Low bids with high interest rates in the range of

13 to 15 per cent make it challenging to borrow in India (most Indian Banks look

at these projects as risky.) and successfully execute a quality project that can

last 25 years. The rating does not include major players such as BHEL, BEL, CEL,

TATA BP Solar India Limited, Solar Semi-conductor & Moser Baer India

Limited, LANCO, L&T, INDO SOLAR, Reliance Power, Mahindra Power, Wipro-ECO

etc. Limited has recently signed Piven by FiTs. By introducing the solar

Renewable Purchase Obligations (RPOs) and the solar Renewable Energy Certificate

(REC) mechanism, the government has created a further market instrument to

advance solar power in India.

The year

will see some movement and interest by market players to explore new business

models/segments within the solar industry in India. Further, the falling cost of

solar will lead to new projects in the captive commercial space as solar tariffs

become competitive with commercial and industrial grid prices in various parts

of the country.

There are also external factors in India challenging its

solar industry, namely high inflation and consequently high interest rates,

slowdown in GDP growth, a several depreciated rupee and relentless corruption

scandals. Low bids with high interest rates in the range of 13 to 15 per cent

make it challenging to borrow in India (most Indian Banks look at these projects

as risky.) and successfully execute a quality project that can last 25 years.

The rating does not include major EPC players such as BHEL,

BEL, CEL, TATA BP Solar India Limited, Solar Semi-conductor & Moser Baer

India Limited, LANCO, L&T, INDO SOLAR, Reliance Power, Mahindra Power,

Wipro-ECO etc.

|