Powering India's Energy Future Amid Storage and Energy Security Challenges

India is witnessing a transformative shift in its energy ecosystem, with rooftop solar installations playing a central role in the nation's renewable energy journey. What began as a small-scale initiative has evolved into a strategic imperative, driving decarbonization, democratization of energy generation, and energy independence. This “rooftop revolution” is fundamentally reshaping the country's energy infrastructure, policies, and business models. However, this rapid growth also presents new challenges, particularly in energy storage and ensuring long-term energy security.

Rooftop Solar: A Rising Pillar of India's Renewable Growth

India's ambitious National Solar Mission and commitments under the Paris Climate Agreement set the foundation for its solar journey. While large-scale solar parks dominate much of the installed capacity, rooftop solar is emerging as an equally significant contributor, particularly in space-constrained urban areas. By leveraging unused rooftop spaces on residential buildings, commercial complexes, and industrial units, rooftop solar provides a decentralized and scalable approach to energy generation.

The economics of rooftop solar have improved dramatically. Plunging module costs, net-metering regulations, and growing awareness of climate change have led to a surge in adoption. Residential users seek relief from high utility tariffs, while businesses and industries view rooftop solar as a cost-control mechanism and a tool for ESG (Environmental, Social, and Governance) compliance. The result is the creation of a new class of energy “prosumers,” generating and consuming electricity simultaneously.

Economic and Environmental Imperatives

For both the economy and the environment, rooftop solar delivers powerful advantages. Distributed generation reduces the need for expensive grid infrastructure expansion and lowers transmission losses. For consumers, the long-term cost savings can be substantial. Meanwhile, India's urban centers benefit from reduced air pollution and carbon emissions as more households and businesses shift to clean energy.

Given India's net-zero target for 2070, rooftop solar adoption is critical. Each kilowatt-hour generated locally displaces coal-based generation, directly contributing to emissions reductions and energy independence. The widespread adoption of rooftop systems can significantly ease the burden on central utilities and accelerate India's journey toward sustainable urbanization.

Policy Support and Market Evolution

Government policy has played a catalytic role in rooftop solar's rise. Capital subsidies for residential installations, net-metering policies, and renewable purchase obligations have incentivized adoption. In parallel, private players have developed innovative business models like the RESCO (Renewable Energy Service Company) model, where third-party developers invest, install, and operate systems, charging users only for the energy consumed.

However, the market is maturing and moving beyond subsidy dependence. Commercial and industrial (C&I) consumers are increasingly motivated by return on investment and long-term energy security. Rooftop installations are also witnessing innovations such as peer-to-peer trading pilots, community solar models, and hybrid solar-plus-storage packages, which make them more attractive.

The Storage Dilemma: Intermittency and Cost Barriers

Despite its success, rooftop solar faces a significant hurdle: its intermittent nature. Solar energy production peaks during daylight hours, often mismatched with residential demand, which rises in the evening. Without effective storage, excess solar generation goes unused or is injected into the grid at low tariffs, diminishing the system's economic value.

Batteries, especially lithium-ion technology, are emerging as the preferred solution. Costs have declined globally, but affordability remains a challenge in India. For many residential users, adding a battery nearly doubles the system cost. Furthermore, lifecycle costs, including replacements every 7–10 years, pose additional financial burdens.

India's reliance on imported lithium and other critical minerals exposes the sector to supply chain disruptions and geopolitical risks. The lack of robust domestic manufacturing adds another layer of vulnerability, making storage one of the most pressing challenges for rooftop solar expansion.

Grid Integration and Technical Complexities

The technical challenges extend beyond storage costs. Distribution networks in most Indian cities were not designed for two-way power flows. High rooftop penetration without adequate storage can cause grid imbalances, voltage fluctuations, and safety risks. Utilities must invest in smart meters, advanced grid monitoring, and automated demand-response systems to accommodate rooftop solar safely.

Energy storage integration also requires intelligent management. Deciding when to store, discharge, or inject power into the grid requires sophisticated software and predictive analytics. Without such intelligence, rooftop systems risk underperforming economically and technically.

Energy Security: Rooftop Solar as a Strategic Asset

Beyond the environmental and economic benefits, rooftop solar has a critical role to play in India's energy security strategy. The nation currently imports a significant portion of its fossil fuels and even some renewable technology components. Global market volatility, geopolitical tensions, and supply chain shocks can leave India vulnerable.

Rooftop solar reduces dependence on centralized fossil fuel-based power and imported energy sources. When paired with storage, it can provide localized energy resilience, ensuring that critical infrastructure like hospitals, schools, and emergency services remain powered during grid outages. During extreme weather events and disasters, decentralized solar-plus-storage microgrids can serve as reliable backup systems, bolstering community resilience.

India's electrification of transportation and digital economy will significantly increase energy demand. Meeting this demand sustainably and securely requires diversified, distributed, and domestically controlled energy sources. Rooftop solar, coupled with indigenous battery manufacturing initiatives under the National Energy Storage Mission and production-linked incentive (PLI) schemes, is a cornerstone of this strategy. Building a robust domestic ecosystem for solar modules, batteries, and related technologies will insulate India from global shocks while creating employment opportunities.

Emerging Solutions: Policy and Technology Pathways

To resolve storage and energy security challenges, multiple strategies are taking shape. The National Energy Storage Mission aims to develop advanced battery technologies and boost domestic manufacturing. Research is also underway on alternative chemistries like sodium-ion and flow batteries, which could reduce reliance on imported lithium.

Dynamic pricing and time-of-day tariffs can incentivize battery adoption, encouraging users to store energy when supply is abundant and discharge during peak hours. Digital energy platforms using AI and IoT can optimize rooftop systems for cost, reliability, and grid support.

Moreover, microgrids and community storage solutions can address affordability barriers. Instead of each household investing in a separate battery, a shared storage facility serving multiple consumers could significantly reduce costs while enhancing grid resilience.

Financing Innovations and Business Models

Financing remains a major barrier to widespread storage adoption. While rooftop solar costs have dropped sharply, adding batteries significantly raises upfront expenditure. Innovative financing is therefore critical. Green bonds, concessional loans from development banks, and battery-leasing or battery-as-a-service models are emerging solutions.

Under long-term power purchase agreements (PPAs), developers can integrate storage without burdening end-users with high capital costs. These models also make rooftop solar attractive for industries and commercial establishments that seek cost predictability and energy resilience.

Urban Potential and Distributed Energy Future

India's urban landscape holds vast untapped rooftop potential. High-rise residential buildings, commercial complexes, industrial parks, hospitals, and educational institutions can all benefit from rooftop solar integrated with storage. Beyond self-consumption, surplus energy can be pooled into local microgrids or traded through peer-to-peer platforms.

The evolution of distributed energy systems will redefine how India produces, distributes, and consumes electricity. In the coming decade, cities could operate on hybrid grids where centralized utilities work in tandem with decentralized generation, enhancing reliability and sustainability.

A Long-Term Vision

The rooftop revolution is not a fleeting trend but an integral part of India's long-term energy transition. Unlocking its full potential requires coordinated action:

Policy Support:

Integrated policies for solar-plus-storage, grid modernization, and domestic manufacturing.

Technology Advancements:

AI-driven energy management, advanced battery chemistries, and smart grid infrastructure.

Consumer Awareness:

Education campaigns to showcase the economic and resilience benefits of rooftop systems with storage.

When aligned, these efforts can transform rooftop solar from an alternative energy source into a mainstream pillar of India's energy security framework.

Conclusion: Towards a Self-Reliant Energy Future

India's rooftop revolution symbolizes the democratization of energy empowering consumers, strengthening grid resilience, and advancing sustainability. However, without solving the storage dilemma and addressing energy security holistically, its true potential cannot be realized.

A progressive and forward-looking strategy that seamlessly integrates widespread rooftop deployment with highly efficient energy storage solutions, advanced smart grid infrastructure, and robust domestic manufacturing capabilities will not only power homes, businesses, and industries but also play a pivotal role in safeguarding India's long-term energy security and future prosperity.

|

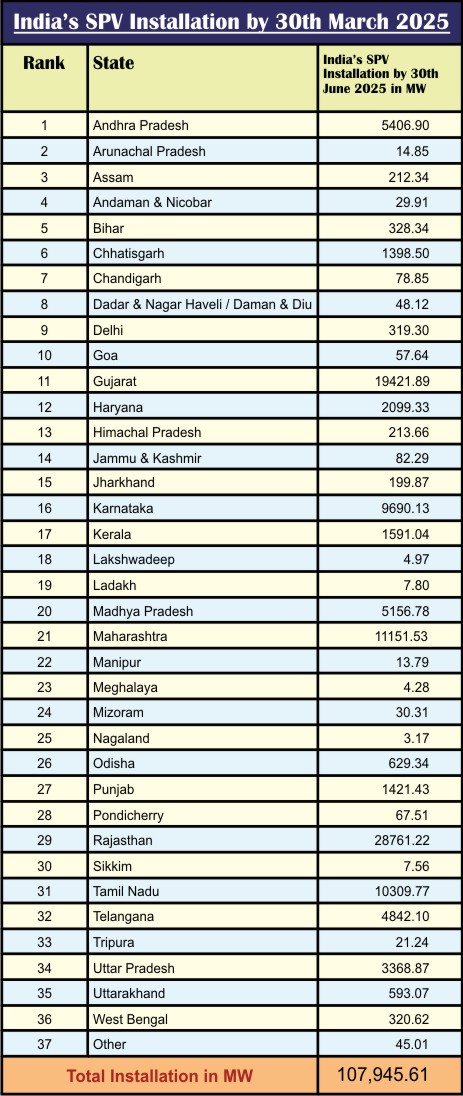

At the forefront of India's solar energy revolution, Rajasthan has consolidated its position as the national leader with an installed grid-connected solar energy capacity of 28.76 GW as of June 30, 2025. This is a remarkable leap from approximately 22.41 GW recorded at the close of the previous fiscal year. The state's abundant sunshine, vast tracts of arid land, and proactive renewable energy policies have together enabled this remarkable expansion. Rajasthan's solar infrastructure serves as a benchmark for other regions aspiring to harness solar energy on a massive scale. Several landmark projects have fueled this growth.

At the forefront of India's solar energy revolution, Rajasthan has consolidated its position as the national leader with an installed grid-connected solar energy capacity of 28.76 GW as of June 30, 2025. This is a remarkable leap from approximately 22.41 GW recorded at the close of the previous fiscal year. The state's abundant sunshine, vast tracts of arid land, and proactive renewable energy policies have together enabled this remarkable expansion. Rajasthan's solar infrastructure serves as a benchmark for other regions aspiring to harness solar energy on a massive scale. Several landmark projects have fueled this growth.